Market Update 04-15-2024

THE BIG PICTURE:

Counting-up of the number of all our indicators that are ‘Up’ for U.S. Equities, the current tally is that all of the four are Positive. These represent a multitude of timeframes:

- LONG-TERM CYCLICAL BULL/BEAR — POSITIVE since April 21, 2023

- MIDTERM/QUARTERLY — POSITIVE since January 1, 2024

- SHORT-TERM — POSITIVE since November 16, 2023

- SHORT-TERM — POSITIVE since November 21, 2023

LAST WEEK IN THE MARKETS

STARTING WITH A DOMESTIC OVERVIEW

INFLATION DISAPPOINTS ON THE UPSIDE IN U.S. AND ON THE DOWNSIDE IN CHINA

The major equity benchmarks retreated for the week amid heightened fears of conflict in the Middle East and some signs of persistent inflation pressures that pushed long-term Treasury yields higher. Large-caps held up better than small-caps, with the Russell 2000 Index suffering its biggest daily decline in almost two months on Wednesday and falling back into negative territory for the year to date. Growth stocks also fared better than value shares, which were weighed down by interest rate-sensitive sectors, such as real estate investment trusts (REITs), regional banks, housing, and utilities.

The primary factor weighing on sentiment appeared to be Wednesday morning’s release of the Labor Department’s consumer price index (CPI) data, which showed headline prices rising by 0.36% in March, right in line with February’s increase, in contrast with consensus hopes for a small decline from the month-earlier pace. A rebound in the price of medical services (from -0.1% in February to +0.6% in March) was partly to blame, as was a continuing sharp rise in transportation services costs, which rose 10.7% over the preceding 12 months, fed largely by increases in the cost of car insurance. Overall inflation rose 3.5% over the preceding 12 months, its biggest gain since September.

U.S. MARKET INDEXES OVERVIEW

The negative momentum continued across the board this week for the indexes with near 3-percent losses for both mid and small-cap. The S&P500 took the least damage, though still losing a near quarter percent of gains for the week.

|

INDEX |

THIS WEEK’S CLOSE |

WEEK’S CHANGE % |

% change ytd |

|

DJIA |

37,983.24 |

-2.37% |

+ 0.71% |

|

S&P 500 |

5,193.56 |

-0.21% |

+ 9.50% |

|

Nasdaq comp. |

16,175.09 |

-0.45% |

+ 9.54% |

|

s&P 400 (midcap) |

2,899.72 |

-2.99% |

+ 4.60% |

|

Rusell 2000 |

2,003.17 |

-2.92% |

- 0.48% |

DOW & TECH

The Dow Jones Industrial Average (DJIA)

is the oldest continuing U.S. market index with over 100 years of history and is made up of 30 highly reputable “blue-chip” U.S. stocks (e.g. Coca-Cola Co., Microsoft).

This week saw the second week in a row of significant losses for DJIA, declining -2.37% to end the week of Apr 12 at 37,983.24 vs the prior week of 38,904.04.

The Nasdaq Composite Index

tracks most of the stocks listed on the Nasdaq Stock Market - the second-largest stock exchange in the world. Over half of all stocks on the NASDAQ are tech stocks.

Continuing its downward streak this week, the tech-driven Nasdaq saw further decline, this week with a loss of -0.45%, closing at 16,175.09 vs. the prior week of 16,248.52. YTD growth is now sub-10%.

SMALL, MEDIUM, & LARGE CAP

The S&P 500 large-cap index

is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S. The S&P 500 is regarded as one of the best gauges of prominent American equities' performance, and by extension, that of the stock market overall.

The S&P 500 finished down again this week, with slower losses than last week, but still declining -0.21%, closing at 5,193.56 vs last week’s close of 5,204.34.

The S&P 400 mid-cap index

is the benchmark index made up of 400 stocks that broadly represent companies with midrange market capitalization between $3.6 billion and $13.1 billion. It is used by investors as a gauge for market performance and directional trends in U.S. stocks.

The S&P 400 mid-cap index saw further gains this week – the heaviest of the list above - declining -2.99% to close at 2,899.72 vs last week’s 2,989.16.

The Russell 2000 (RUT) small-cap index

measures the performance of the 2,000 smaller companies included in the Russell 3000 Index. The Russell 2000 is managed by London's FTSE Russell Group and is widely regarded as a leading indicator of the U.S. economy because of its focus on smaller companies that focus on the U.S. market.

For a second week in a row, the Russel 2000 saw near 3% losses, declining -2.92% and closing at 2,003.17 vs last week’s close of 2,063.47. This puts RUT into a negative state for the year-to-date.

U.S. COMMODITIES / FUTURES OVERVIEW

Gold, silver, and copper all fared better this week while the indexes suffered. Copper saw a near 2% lift over the prior week while Crude Oil declined almost a percent and a half after a lift toward the end of the market week.

|

INDEX |

CLOSE 4/5/24 |

CLOSE 4/12/24 |

WEEK’S CHANGE % |

% change ytd |

|

GOLD |

2,349.10 |

2,360.20 |

0.47% |

13.83% |

|

SILVER |

27.60 |

27.97 |

1.34% |

16.78% |

|

Copper |

4.24 |

4.32 |

1.89% |

11.34% |

|

crude oil |

86.73 |

85.45 |

-1.48% |

21.41% |

ECONOMIC NEWS

FOR THE U.S. MARKET

SUPERCORE INFLATION HITS HIGHEST LEVEL IN ALMOST A YEAR

More concerning may have been a material increase in so-called supercore inflation, which tracks services prices excluding energy and housing costs, which policymakers have acknowledged are a lagging indicator of overall inflation trends. Supercore inflation jumped 0.7% in March and 4.8% over the past 12 months, substantially higher than expectations and its biggest increase in 10 months.

In the wake of the report, futures markets began pricing in roughly a 20% chance of a rate cut at the Federal Reserve’s June policy meeting versus roughly 50% before its release. The week was a busy one for commentary from central bank officials, with 11 scheduled to speak, according to traders, and they seemed to confirm a change in their perspective following the CPI release. In particular, Richmond Fed chief Thomas Barkin said that the latest data did not increase his confidence in disinflation, and Boston Fed President Susan Collins said that the recent data argue against an imminent need to cut rates.

Thursday’s release of producer price inflation data seemed to help calm inflation fears and help equity markets recoup a portion of their losses. Producer prices rose 0.2% in March, a tick below expectations and well under February’s 0.6% increase. Input goods prices fell 0.1%, continuing a recent pattern of goods deflation that had been interrupted by a 1.2% surge in April.

REPORTS OF IMMINENT STRIKE ON ISRAEL SEND INVESTORS FLOCKING TO OIL AND U.S. DOLLAR. Stocks pulled back sharply to end the week, however, in the wake of reports that Iran was preparing to directly attack facilities on Israeli soil for the first time. Oil prices rose on the news, along with the U.S. dollar, which is typically viewed as a “safe haven” in times of international turmoil. Meanwhile, the CBOE Volatility Index (VIX), Wall Street’s so-called fear gauge, spiked to its highest level since November.

The consumer inflation data helped drive the yield on the benchmark 10-year U.S. Treasury note to its highest intraday level since November before Treasuries rallied on Friday as investors sought out U.S. dollar-based assets. (Bond prices and yields move in opposite directions.) Traders noted a cautious tone in the tax-exempt municipal bond market as investors were expected to liquidate some holdings ahead of the April 15 tax deadline. Both investment-grade and high-yield corporate bonds wavered following the CPI report, but issuance appeared to be met with continued healthy demand.

LAST 52 WEEKS OF THE VOLITILIY INDEX (VIX)

VIX closed at 17.31 this week, a 7.99% increase over last week’s close of 16.03. This continues to be a possible indication that there’s more demand and options prices may start to increase.

*see footnotes for more information on VIX

THE CAPE THIS YEAR (2024)

34.02 – down this week 1.53% from last week’s value of 34.55

|

CAPE VALUE |

DATE |

% change |

% change ytd |

|

31.19 |

JAN 1, 2024 |

— |

— |

|

33.55 |

FEB 1, 2024 |

+ 7.57% |

+ 7.57% |

|

34.21 |

MARCH 1, 2024 |

+ 1.97% |

+ 9.68% |

|

34.66 |

APRIL 1, 2024 |

+ 1.32% |

+ 11.13% |

|

34.02 |

APRIL 12, 2024 |

- 1.53% |

+ 9.07% |

CAPE = cyclically adjusted price-to-earnings ratio (CAPE)

Note: We do not use CAPE as an official input into our methods. However, we think history serves as a guide and that it’s good to know where we are on the historic continuum.

INTERNATIONAL MARKETS

LOOKING AT THE BROADER PICTURE

|

GLOBAL EXCHANGE/index |

week CLOSE |

% change WEEK |

% change ytd |

|

CANADA - TSX |

21,899.99 |

- 1.64% |

+ 4.92% |

|

UK – FTSE 100 |

7,995.58 |

+ 1.07% |

+ 3.55% |

|

FRANCE – CAC 40 |

8,010.83 |

- 0.63% |

+ 6.37% |

|

GERMANY - DAX |

17,930.32 |

- 1.35% |

+ 6.92% |

|

CHINA – SHANGHAI COMP. |

3,019.47 |

- 1.62% |

+ 1.93% |

|

JAPAN – NIKKEI 225 |

39,523.55 |

+ 1.36% |

+ 18.73% |

EUROPEAN OVERVIEW

In local currency terms, the pan-European STOXX Europe 600 Index ended 0.26% lower. Major stock indexes also fell. Germany’s DAX lost 1.35%, France’s CAC 40 Index declined 0.63%, and Italy’s FTSE MIB slid 0.73%. However, the UK’s FTSE 100 Index bucked the downtrend, gaining 1.07%. The British pound’s weakness relative to the U.S. dollar helped support the index, which includes many multinationals that generate meaningful overseas revenue.

After trending lower early in the week, yields on French, German, and Italian government bonds jumped on news that U.S. inflation had accelerated faster than expected in March. Yields subsequently pulled back from these highs as the European Central Bank (ECB) held key rates steady but hinted strongly that it might lower them soon. UK bond yields rose, lifted in part by hawkish comments from Bank of England policymaker Megan Greene, who warned that “rate cuts should still be a way off.”

ECB POINTS TO JUNE RATE CUT

The ECB left its key deposit rate at a record high of 4.0%, as expected, but said that if an updated inflation assessment, which is due in June, “were to increase its confidence that inflation is converging to the target in a sustained manner, it would be appropriate to reduce the current level of monetary policy restriction.” Asked if the strong U.S. inflation data would affect the policy path, she replied that the ECB was “data-dependent, not Fed-dependent” and that U.S. and eurozone inflation were “not the same.”

UK ECONOMY GROWS FOR TWO MONTHS IN A ROW

UK gross domestic product (GDP) in February expanded 0.1% sequentially, thanks to a rebound in manufacturing output. The Office of National Statistics also revised January GDP growth 0.3% from 0.2%, suggesting the economy exited recession. In the three months through February, gross domestic product expanded 0.2%.

EUROZONE CONFIDENCE RISES; GERMAN OUTPUT UP AGAIN

Investor confidence in the eurozone rose in April to its highest level in more than two years, according to an index compiled by Sentix. The economic expectations barometer turned modestly positive for the first time since Russia invaded Ukraine.

In Germany, industrial production in February rose 2.1% sequentially, the second consecutive month of strong gains, due to increased construction output. However, in the three months through February, production was 0.5% lower than in the previous period.

JAPAN

Japan’s stock markets gained over the week, with the Nikkei 225 Index up 1.4% and the broader TOPIX rising 2.1%. As the Japanese yen hovered close to a 34-year low, investors’ focus was on whether the country’s authorities would step in to support the currency.

Following a hot U.S. inflation print and subsequent rise in U.S. Treasury yields, the 10-year Japanese government bond yield rose to 0.84%, from 0.77% at the end of the previous week. It briefly touched its highest level since November 2023 during the week.

YEN BREACHES KEY LEVEL, BUT NO INTERVENTION YET BY AUTHORITIES

The yen weakened from the high-JPY 151 range against the U.S. dollar level to beyond the 152 level that many investors have come to regard as the point at which Japanese authorities could be expected to intervene in the foreign exchange markets to prop up the currency. No such intervention was forthcoming during the week, although finance ministry authorities stated that they were looking at the factors behind the currency moves and that they would act on excessive yen weakness.

BANK OF JAPAN RULES OUT RESPONDING TO YEN WEAKNESS WITH RATE HIKE

Bank of Japan (BoJ) Governor Kazuo Ueda, in turn, ruled out responding to a weak yen with a rate hike. He emphasized that the central bank would not change its monetary policy directly in response to exchange rate moves. The BoJ recently ended its negative interest rate policy and unwound its program of yield curve control, in response to signs that prices were rising in tandem with wages, a stated precondition for monetary policy tightening. Market expectations now appear to have converged around two further rate hikes within a one-year period.

It is worth noting that Japan’s monetary policy remains among the most accommodative in the world, and expectations are that financial conditions will also remain accommodative for the time being. A combination of historic weakness in the yen and accommodative monetary policy provide a favorable backdrop for Japan’s stock indexes, where many of the largest constituents are exporters deriving a sizable share of their earnings from overseas.

CHINA

Chinese stocks retreated as weak inflation data underscored the lackluster demand hanging over China’s economy. The Shanghai Composite Index declined 1.62%, while the blue chip CSI 300 gave up 2.58%. In Hong Kong, the benchmark Hang Seng Index ended nearly flat from last week after apprehensions about the flagging recovery pared earlier gains.

China’s consumer price index rose a below-consensus 0.1% in March from a year earlier, down from February’s 0.7% rise, as food costs retreated following a brief increase during the Lunar New Year holiday in February. Core inflation rose by 0.6% but was weaker than February’s 1.2% increase. Meanwhile, the producer price index fell 2.8% from a year ago, marking its 18th month of declines and accelerating from February’s 2.7% drop.

TRADE DATA FALL MORE THAN EXPECTED

China’s exports and imports fell in March and reversed gains from the first two months of the year. Exports shrank a worse-than-expected 7.5% in March from a year ago compared with a 7.1% rise in the January to February period. Meanwhile, imports dipped 1.9%, down from 3.5% growth in the first two months of the year. The latest results dealt a setback to China’s reliance on external demand to bolster its economy and added pressure on Beijing to ramp up stimulus measures as it tries to achieve its 5% annual growth target set at the National People’s Congress in March.

HIGHLIGHT OF THE WEEK:

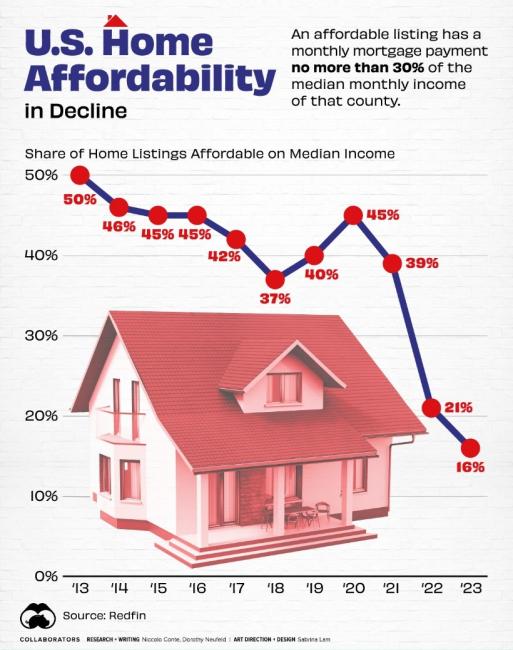

Visualizing America’s Shortage of Affordable Homes

https://www.visualcapitalist.com/americas-shortage-of-affordable-homes/

A large share of affordable homes vanished over the pandemic, leading the supply to hit its lowest level on record in 2023. Many buyers have become priced out of the market due to soaring home prices and high interest rates.

Last year alone, the number of affordable homes shrank by almost 41%, equal to over 243,000 properties.

The graphic below shows the dwindling supply of affordable U.S. homes, based on data from Redfin. In 2023, only 16% of homes were affordable in America, falling from 21% in the year before.

An affordable listing was defined as one with a monthly mortgage payment no more than 30% of the median monthly income of that county. Below, we show the share of affordable listings in the 97 biggest U.S. metropolitan areas by population:

|

YEAR |

SHARE OF AFFORDABLE HOME LISTINGS |

U.S. MEDIAN SALE PRICE ON NEW HOME |

AVERAGE 30-YEAR FIXED MORTGAGE RATE |

|

2023 |

16% |

$427,400 |

6.81% |

|

2022 |

21% |

$457,800 |

5.34% |

|

2021 |

39% |

$397,100 |

2.96% |

|

2020 |

45% |

$336,000 |

3.10% |

|

2019 |

40% |

$321,500 |

3.94% |

|

2018 |

37% |

$326,400 |

4.54% |

|

2017 |

42% |

$323,100 |

3.99% |

|

2016 |

45% |

$307,800 |

3.65% |

|

2015 |

45% |

$294,200 |

3.85% |

|

2014 |

46% |

$288,500 |

4.17% |

|

2013 |

50% |

$268,900 |

3.98% |

As the above table shows, housing affordability has grown increasingly out of reach as mortgage rates have more than doubled in just two years.

While affordable homes made up 39% of the market in 2021, the share dropped precipitously as interest rates climbed higher. In 2023, the average annual 30-year fixed mortgage rates reached 6.81%—hitting its highest level in 20 years.

Although mortgage rates may decline over the year if the Federal Reserve cuts interest rates, it may not be enough to boost the supply of affordable housing.

That’s because rates may not fall sharply enough to undo the “golden hand-cuff” effect, where homeowners are reluctant to sell in order to hold on to their low mortgage rates. Adding to this, home construction has fallen significantly since the global financial crisis. During this time, home builders and lenders became increasingly cautious, leading home construction to drop 55% between 2006 and 2021.

WHAT COMES NEXT? The good news is that new-home construction is forecast to increase in 2024, with single-family housing starts projected to grow 4.7%.

While new home sales have historically comprised 10-12% of the single-family home market, they have recently surged to 30% due to the collapsing supply of existing homes. But even as new supply enters the market, it will likely take a number of years for housing affordability return to historical levels. In fact, JP Morgan suggests that it could take two years if mortgage rates drop by 1 percentage point, assuming that home prices remained at all-time highs and wages continued rising at their current pace.

-------------------------

HOW VIX WORKS

The Volatility Index or VIX is the annualized implied volatility of a hypothetical S&P 500 stock option with 30 days to expiration. It can help investors estimate how much the S&P 500 Index will fluctuate in the next 30 days. While the VIX only measures the volatility of the S&P 500 Index, it has become a benchmark for the U.S. stock market.

The VIX is often referred to as the market’s “fear index or fear gauge”. The performance of the VIX is inversely related to the S&P 500 – when the price of the VIX goes up, the price of the S&P 500 usually goes down.

If the VIX is rising, demand for options is increasing, and therefore, becoming more expensive. If the VIX is falling, there's less demand, and options prices tend to fall. One thing to keep in mind is that current volatility cannot be known ahead of time. That's why it's a good idea to use the VIX in tandem with technical and fundamental analysis.

------------------------

HOW CAPE WORKS

The cyclically adjusted price-to-earnings ratio (CAPE) can be used to smooth out the shorter-term earnings swings to get a longer-term assessment of market valuation. An extremely high CAPE ratio means that a company’s stock price is substantially higher than the company’s earnings would indicate and, therefore, overvalued. It is generally expected that the market will eventually correct the company’s stock price by pushing it down to its true value.

In the past, the CAPE ratio has proved its importance in identifying potential bubbles and market crashes. The historical average of the ratio for the S&P 500 Index is between 15-16, while the highest levels of the ratio have exceeded 30. The record-high levels occurred three times in the history of the U.S. financial markets. The first was in 1929 before the Wall Street crash that signaled the start of the Great Depression. The second was in the late 1990s before the Dotcom Crash, and the third came in 2007 before the 2007-2008 Financial Crisis.

https://www.multpl.com/shiller-pe

---------------------------------

Sources: All index and returns data from Norgate Data and Commodity Systems Incorporated and Wall Street Journal. News from Reuters, Barron’s, Wall St. Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, visualcapitalist.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet, Morningstar/Ibbotson Associates, Corporate Finance Institute